Presented by Meyers Nave, this edition of San Diego’s Data Bites covers September 2021, with data on employment and more insights about the region’s economy at this moment in time. Check out EDC’s Research Bureau for even more data and stats about San Diego.

KEY TAKEAWAYS

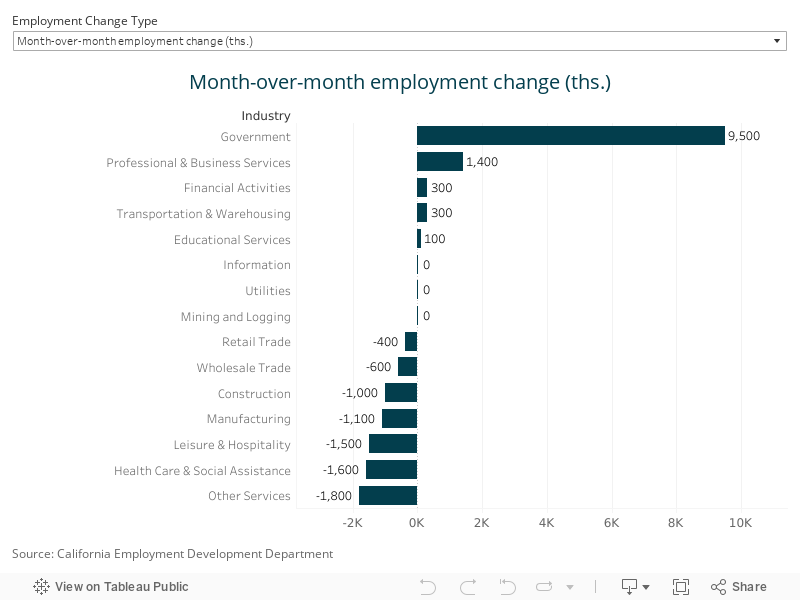

- San Diego establishments added a meager 3,600 payroll positions between August and September, all of which came from the public sector as teachers and school staff were brought back on.

- The unemployment rate tumbled to 5.6 percent in September from August’s 6.6 percent. However, the improvement is out of step with the payroll job counts and may not withstand data revisions.

- Inflation in San Diego has been running even hotter than the national average in recent months. However, fundamentals suggest price pressures will ease by next Spring.

A lackluster report

San Diego establishments added a meager 3,600 payroll positions between August and September, all of which came from the public sector as teachers and school staff were brought back on. A build of 9,500 government positions was partially offset by the loss of 5,900 private-sector jobs. Losses in Other Services—which include gyms and salons—gave up 1,800 positions, followed by a loss of 1,500 in Leisure and Hospitality, potentially spotlighting the impacts of the Delta and Mu COVID-19 variants on the job market.

While the employment report is typically referenced as a single data point, it is actually an agglomeration of two separate surveys: (1) the establishment survey, which is used to measure the number of payroll jobs gained or lost in a given month, and (2) the household survey that provides information on the labor force and is used to calculate the unemployment rate. Typically, these two surveys line up pretty well, but last month was an exception. The separate household survey revealed that the jobless rate dropped a full percentage point from 6.6 percent in August to a post-pandemic low of 5.6 percent last month. That said, the improvement is out of step with the payroll jobs count and relies on a much smaller sample size. As such, last month’s decline in unemployment may not withstand revisions, and future reports may indicate a higher jobless rate in the region.

Inflation concerns are overinflated

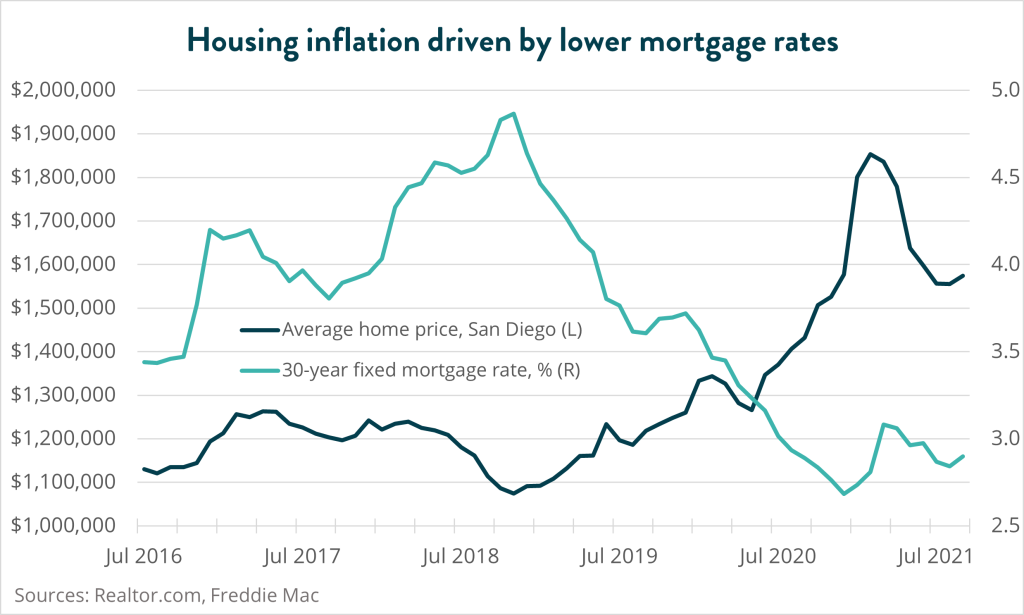

The economy is dealing with an issue that it hasn’t had to in quite a while: inflation. The U.S. Bureau of Labor Statistics (BLS) recently reported that the widely watched consumer price index (CPI) increased 5.4 percent from September 2020 to September 2021, the fastest year-over-year rise since July 2007 to 2008. Closer to home, consumer prices in San Diego County rose at an even brisker 6.5 percent during that time, the second highest rate of inflation among a group of 12 metro areas reported for September behind only Riverside CA. Much of this can be attributed to a sharp rise in housing costs.

As of August, San Diego house prices were up 26 percent from a year ago, but this is due in large part to two phenomena: (1) lower mortgage rates, and (2) people taking advantage of lower house prices in East County. Mortgage rates are responsible for 70 percent of San Diego house price fluctuations, about double the national average. A brief rise in borrowing costs paused the climb in home values in the late Spring, but it will take a more convincing rise in rates to bring property values back to Earth. This should begin in early 2022 after the Federal Reserve starts to normalize monetary policy.

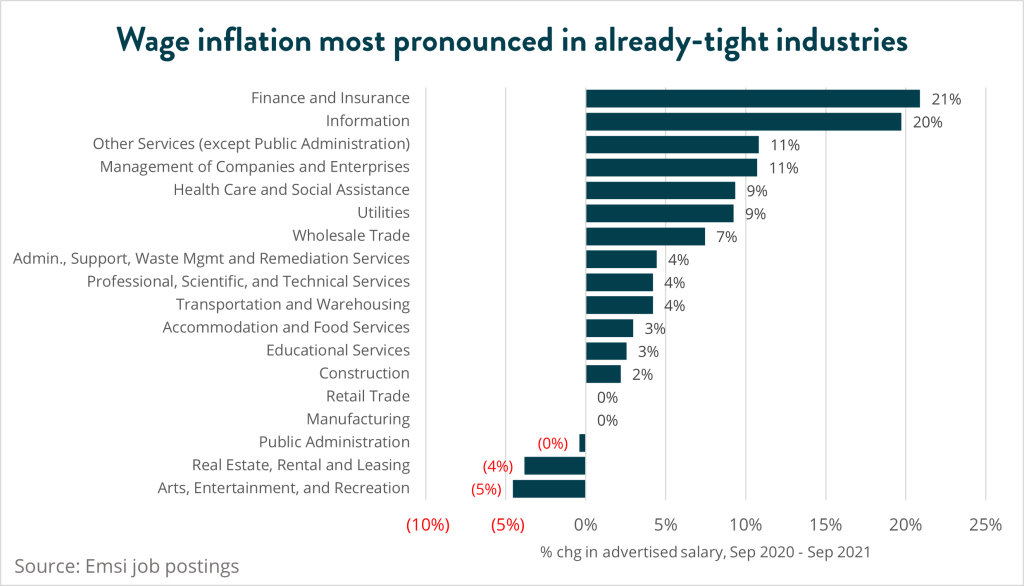

Wage growth presents the biggest hurdle to quelling inflation in the near term. According to Emsi, advertised salaries for open positions in San Diego were up 4.9 percent in September 2021 from a year earlier as employers hunt for scarce talent. For context, that rise was nearly double the average rate of 2.5 percent observed between 2010 and 2019 but about half the 9.7 percent increase observed in 2020. Given the deceleration from 2020, it would already appear that wage inflation pressures are subsiding.

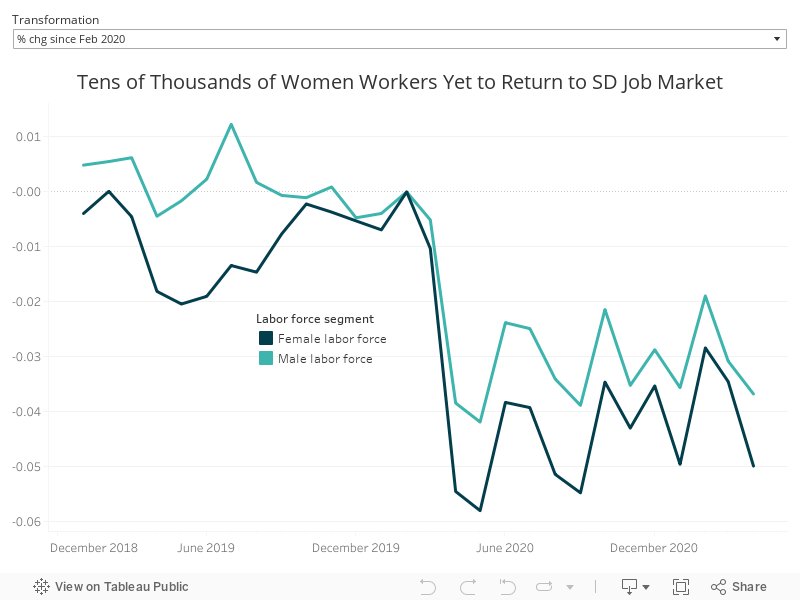

It remains to be seen whether rising wages will be enough to bring people back to the workforce. More than 50,000 San Diegans are yet to return to the job market, and much of the increase in wages over the past year is attributable to a handful of industries that were struggling to source talent even before the pandemic. Finance and insurance companies are advertising salaries that are 21 percent higher than they were in September 2020, while information firms are paying 20 percent more to fill open positions. Yet salaries for Accommodation and Food Services positions are only up three percent.

One in four positions to be recovered in the region are in Accommodation and Food Services, so it could take a more convincing pay boost to bring people back. While this would immediately lead to more wage inflation, it would alleviate inflation in the medium to long term, since an influx of workers would reduce the need for companies to bid up wages.

Taken together, fundamentals suggest that inflation will subside in coming months. The big question is whether people will return to the job market. The combination of rising wages, falling COVID-19 case numbers, and kids returning to the classroom should spur more folks to come back to work. However, as has been the case since March 2020, it will be the virus that dictates how these events unfold. Any rise in San Diego’s COVID-19 numbers could keep people away from jobs that require close personal contact, and this will hurt companies in service industries that pay lower wages and typically don’t provide health benefits the most.