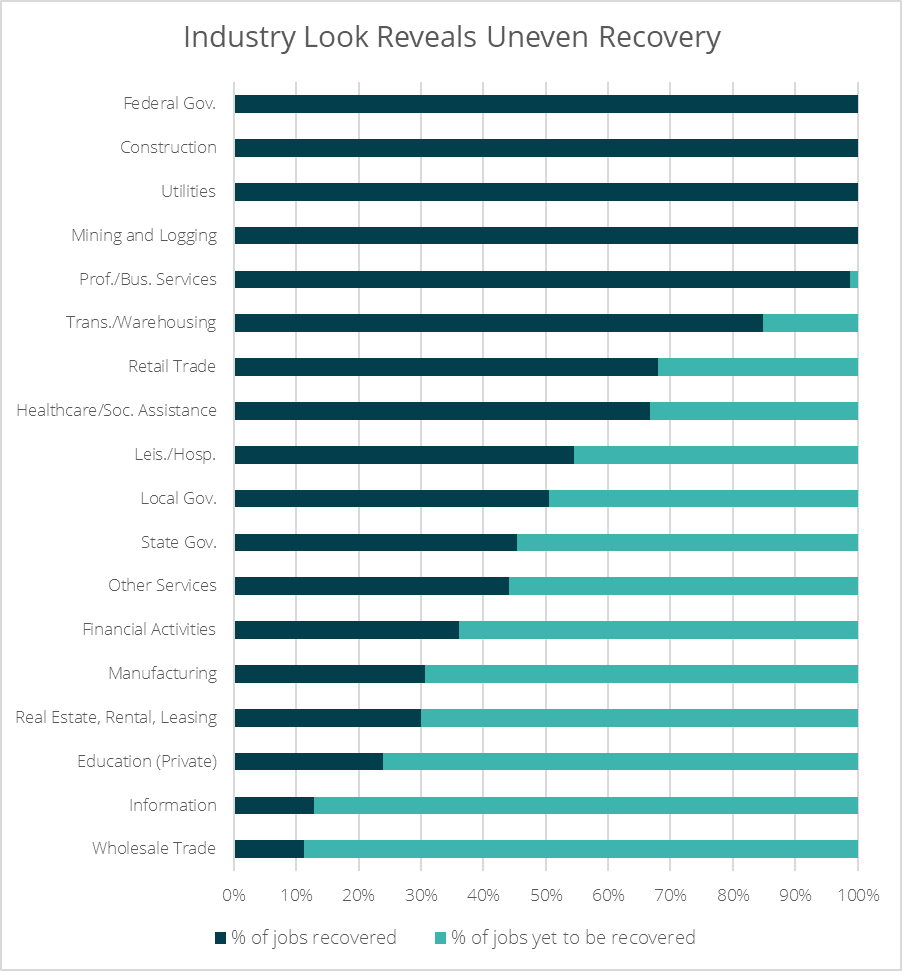

KEY TAKEAWAYS

- Despite ongoing economic pressure, San Diego home values and rents reached new peaks in October.

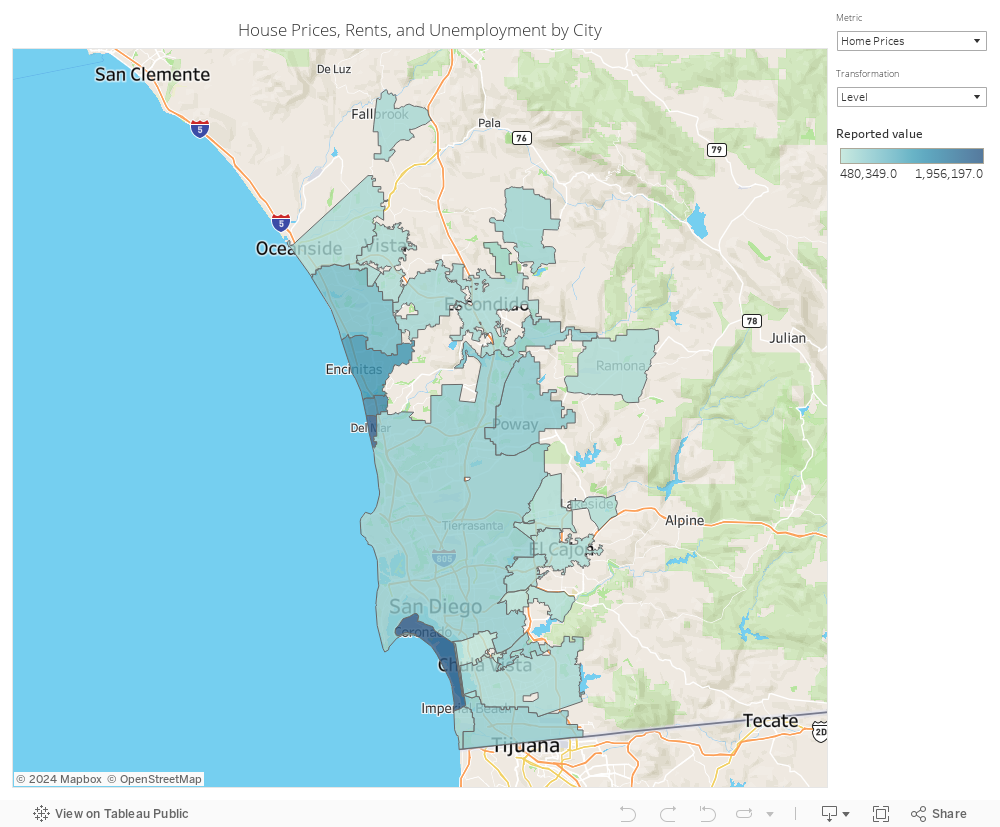

- Home prices and rents are highest along the coast, but price increases have been most pronounced in more rural, inland areas of the county.

- Areas in the county with the highest unemployment rate tend to have the lowest cost of living, however prices are increasing quickest in those areas.

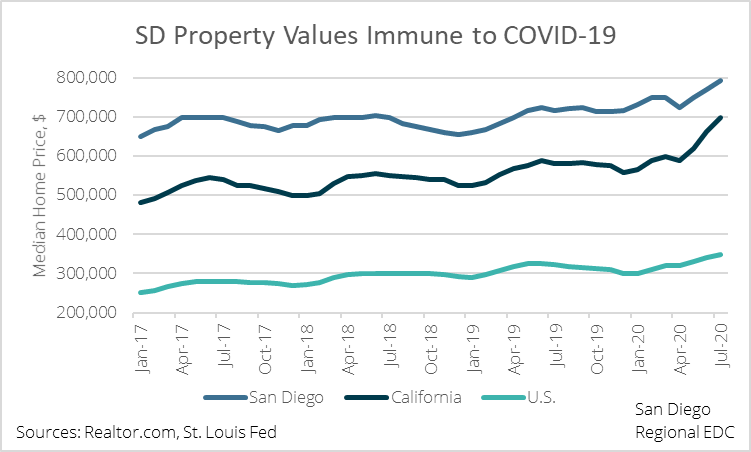

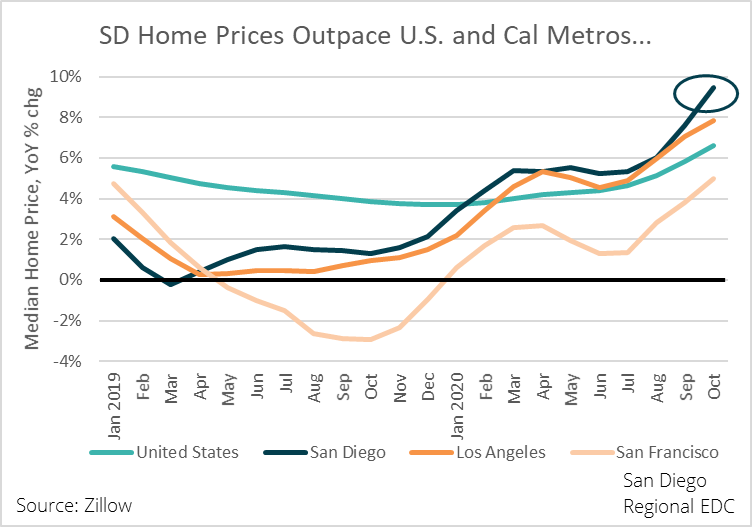

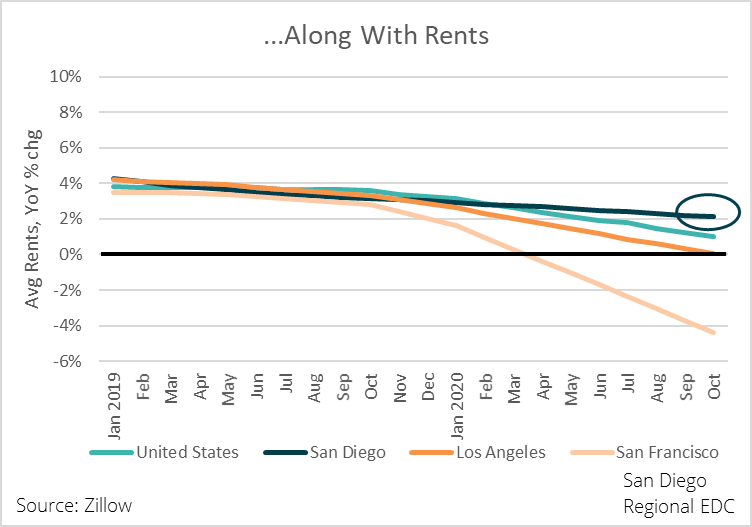

San Diego home prices and rents continued to rise in October, despite the ongoing economic pressures presented by Covid-19 and efforts to contain the virus. According to Zillow, the median value of a middle-tier home advanced 1.6 percent from September to reach a new peak of $649,474*, up 7.3 percent from February and up 9.5 percent from a year ago. Meanwhile, average rents reached $2,363, also a fresh high, up 1.4 percent from February and 2.1 percent from a year earlier.

San Diego home prices and rents are both growing faster than other large California metro areas like San Francisco, Los Angeles, and Santa Barbara, as well as the U.S. average. Even so, San Diego’s record-breaking house prices and rents are not unique. Of the 914 metropolitan and micropolitan regions covered, Zillow reported new home price peaks in 645 (71 percent) of them, and rents are topping out in 88 percent of 107 regions tracked by the real estate company.

Sub-regional look presents an interesting picture

Housing price appreciation has been most pronounced in largely rural areas. Jacumba home values have surged by more than 23 percent over the past year, while prices in Ranchita, Tecate, and Warner Springs are all up between 18 and 19 percent. Yet, the median price for a home in Downtown has inched higher by a much less impressive 2.7 percent year-over-year.

A similar trend plays out when looking at rental values within the county. Rents in Ramona have jetted 15.8 percent higher over the past year, while Escondido rents are up some 6.5 percent. Coincidentally, rents have fallen in more central locations like University City, Carmel Valley, and Downtown.

Generally speaking, housing price appreciation and rental increases are most pronounced in areas where prices and rents are relatively low. This could reflect a natural migration out and away from the City of San Diego as buyers are seeking out price deals in more affordable, inland areas. This is especially true as those who are able to work from home no longer have to weigh as heavily the idea of a longer commute when deciding where to buy.

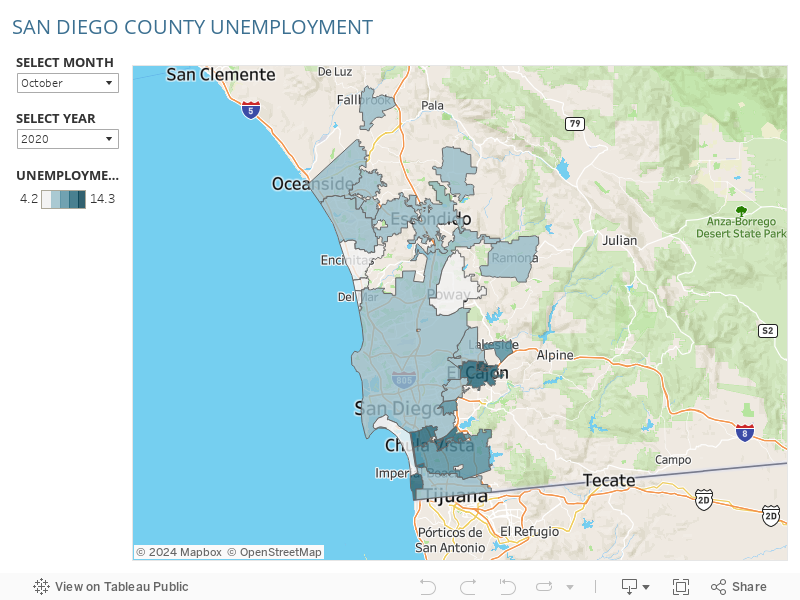

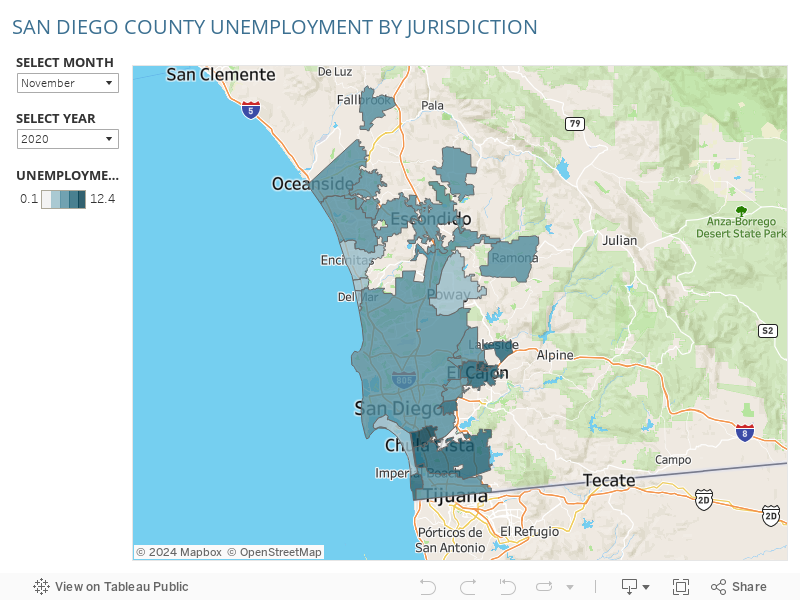

Also worth noting, is that home values and rental prices coincide with economic outcomes in these areas. For example, in Solana Beach, the median home price is more than $1.5 million, and the unemployment rate is just 4.2 percent—well below the county rate of 7.7 percent. By contrast, the median home price is $480,349 in National City, where unemployment is stuck at 11.5 percent. Similarly, rents are topping out at nearly $3,300 per month in low-unemployment Solana Beach, while renters are paying just over $1,800 per month in El Cajon where the jobless rate hovers at 11.4 percent.

The map below clearly shows how home prices and rents are growing in areas where properties are cheaper. Those regions are also the pockets of the county where joblessness is rampant.

Select between home prices, rents, and unemployment below using the ‘Metric’ dropdown, and choose between Level and YoY % change in the ‘Transformation’ dropdown to explore more.

ARE POORER SAN DIEGANS BEING PRICED OUT?

The relationship between home values (an indicator of how much workers in an area can afford) and labor market outcomes during the Covid-19 downturn shines a harsh light on the economic disparities affecting San Diegans with different socioeconomic backgrounds. Workers in areas where home values and rents are lower are far and away more likely to be without a job as Covid-related restrictions force business closures throughout the county.

This relationship statistically significant, offering up yet another piece of hard evidence that the most recent recession has disproportionately hurt poorer people.

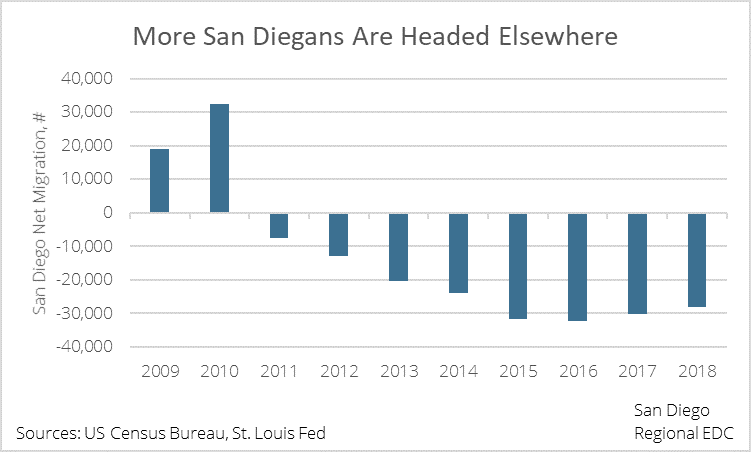

What’s worse is that the torrid pace of price growth for homes and rental properties in higher-unemployment regions may force the most vulnerable San Diegans out of those areas as prices become unaffordable. This would exacerbate an already-troubling trend that has pushed more people out of the region than into it over the past decade.

Now, more than ever, we need to analyze our options and develop policies that help to prevent San Diegans from being priced out of the region. Cultivating and retaining a strong local workforce isn’t just about maintaining San Diego’s identity, it’s also about creating a stronger, more resilient region in coming years that will be better able to withstand the inevitable next downturn. Go here to learn more about how EDC is working to ensure San Diego gets this recovery right.

*Due to availability of data and varying sources, these numbers differ slightly from others we’ve recently posted.