Every quarter San Diego Regional EDC analyzes key economic indicators that are important to understanding the regional economy and the region’s standing relative to the 25 most populous metropolitan areas in the U.S.

EDC explains San Diego’s Q3 2021 economic data:

Key Findings from Q3 2021:

VENTURE CAPITAL: Life Sciences and Tech companies continue to shine. San Diego experienced another phenomenal quarter for VC, reaching $1.9 billion, an increase of $52 million compared to Q2, and $1.1 billion more than the same quarter last year. Life Sciences companies attracted almost $1 billion via 23 deals, with Genomatica pulling in $118 million alone. Twenty Tech companies brought in more than $940 million, with Shield AI and Wiliot attracting $410 million combined.

COMMERCIAL REAL ESTATE: Demand for office and industrial space continues to climb. For the second quarter in a row, San Diego showed positive net absorption of office real estate, pushing vacancy rates down and rents up. The delivery of Amazon’s 3.4 million square-foot warehouse in Otay Mesa led to net absorption of more than 4.7 million square feet of industrial space, the strongest quarter on record.

EMPLOYMENT: San Diego continues to ride the wave of employment gains. Total nonfarm employment increased by 6,200 during Q3 and is up 51,300 compared to a year ago. However, gains were choppy across industries. Leisure and Hospitality led employment growth in Q3 with 7,900 jobs, as Accommodation and Food Services establishments continue to re-open and re-hire. Professional and Business services also had a positive quarter, adding 3,200 jobs to the region as venture funding fuels growth.

Welcome to the fourth edition in EDC’s Changing Business Landscape Series, which will be published bi-monthly in the San Diego Business Journal and here on our blog. If you missed them, check out the March, May, and July editions.

Surveying the changing business landscape in San Diego

The COVID-19 pandemic has impacted every facet of life, including how businesses operate. Companies in every industry are rapidly re-evaluating how they do business, changing the way they interact with customers, manage supply chains and where their employees are physically located. This has massive immediate and long-term implications for San Diego’s workforce and job composition, as well as regional land use decisions and infrastructure investment.

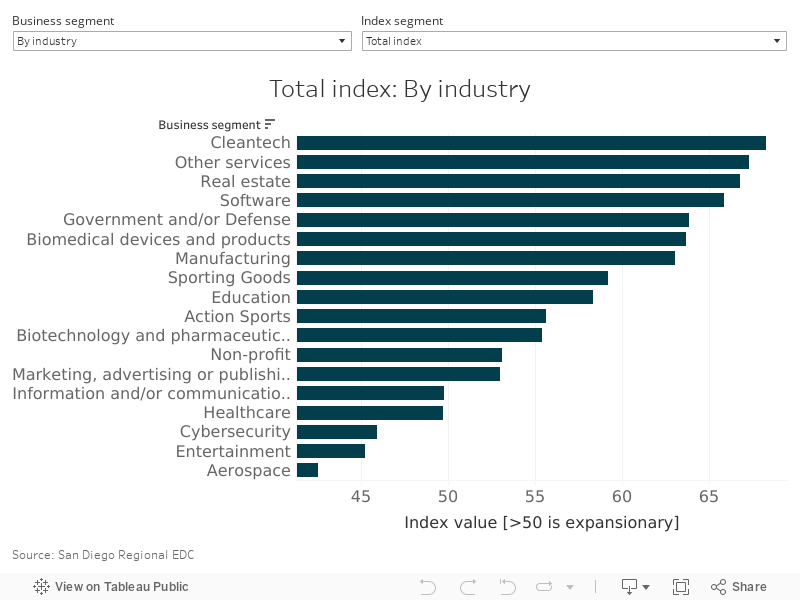

To identify evolving trends in local business needs and operations, ensuring their ability to grow and thrive in the region, San Diego Regional EDC is surveying nearly 200 companies in the region’s key industries on a rolling basis throughout 2021 to monitor and report shifts in their priorities and strategies. In addition, EDC constructed the San Diego Business Recovery Index (BRI)—a sentiment index to measure companies’ perceptions of current conditions, as well as expectations for the future across several factors such as business development, employment, and commercial real estate needs. (An index value >50 reflects expansion, and a value <50 reflects contraction. More information on the index and how it is calculated is available here.)

These insights will help inform long-term economic development priorities around talent recruitment and retention, quality job creation and infrastructure development. Companies are surveyed on several topics, with varying emphases in each wave.

Here are three key findings from the fourth wave of surveying conducted in August 2021:

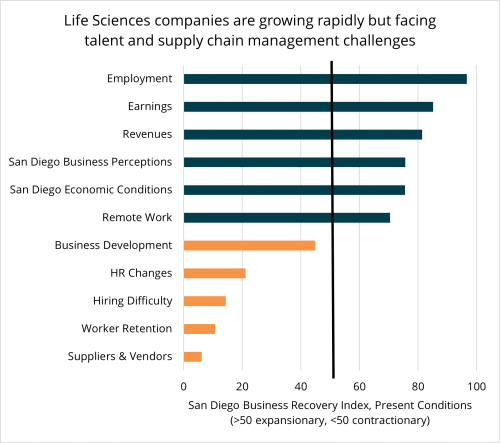

Life Sciences companies struggle to keep pace. Employers reported higher earnings and headcount but also increased difficulty attracting and retaining talent

Supply chain disruptions hurt business development. The more profound impact of prolonged supply chain issues may be on San Diego business operations not local consumers.

Remote work is driving companies to scale down office space. Life Sciences and Manufacturing are the exception, where rising sales and increased staffing will require companies to add space.

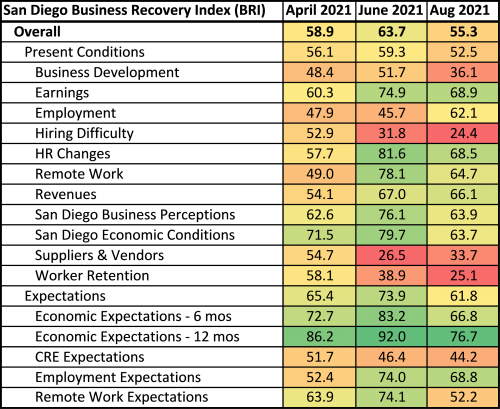

The BRI slid 8.4 points in August to settle at 55.3 after coming in at a solid 63.7 in June. August’s read suggests that the recovery could be slowing and reflects deteriorating views of present business conditions and slightly less upbeat expectations for the next six to 12 months.

All but two subindex values declined in August. The renewed challenges faced by businesses led many to temper their future expectations somewhat, though the expectations subindex remained comfortably in expansionary territory at 61.8. While companies still anticipate an improving local economy over the next six to 12 months, the economic expectations subindex for six months out fell 16.4 points from 83.2 in June to 66.8 in August. Meanwhile, the subindex for economic conditions 12 months out fell 15.3 points from an exuberant 92.0 to a more measured but still optimistic value of 76.7.

Life Sciences companies struggle to keep pace

Employers surveyed reported an acceleration in hiring; the first time the employment subindex moved into expansionary territory. While this is welcome news, employers also reported increased difficulty hiring new workers. Though much attention has been given to the suggestion that extended unemployment benefits are keeping the unemployed from returning to work, the data doesn’t seem to support it. In fact, many of the pre-pandemic hiring trends have persisted and the industries having the hardest time filling jobs are those that are high-skill and high-paying. There were more than 118,000 unique job postings across the region during the month of August. The top job posting industries fall into the Tech and Life Sciences clusters and the most posted occupation was Software Developer (yet again).

San Diego Life Sciences companies have been struggling to add talent fast enough. These companies have been at the forefront of developing treatments and producing medical devices aimed at combatting COVID-19. As such, they have grown rapidly, drawing more than $9 billion in venture capital funding since the pandemic began. While Life Sciences companies reported higher revenues, earnings and employment relative to before the pandemic began, they also report the greatest difficulties filling new positions, keeping their highly in-demand talent from competitors, and dealing with suppliers and vendors. Despite these challenges, most have great expectations for the year ahead, with plans for increasing staff, their physical footprint and remote work capabilities.

Supply chain disruptions hurt business development

One of the longest lasting impacts of the pandemic has been on global supply chains. Companies across the country remain light on inventory even as demand for goods from furniture and clothing to recreational goods and electric bicycles has jumped. In San Diego, consumer spending is now up 11 percent compared to February 2020 before any COVID-related shutdowns began. Many consumer goods are manufactured overseas, and as the Delta variant has spread in many parts of Asia, production has slowed or even halted. While supply chain disruptions may be affecting what San Diegans can buy and the prices they will pay, the more profound impact may be in what San Diego companies can sell and to whom.

Across all industries, San Diego companies noted continuing difficulties with managing suppliers and vendors. From Aerospace and Manufacturing to Software and Life Sciences, supply chain struggles have become more disruptive throughout the summer months. Upstream labor shortages have reduced production, port and travel delays led to late or canceled shipments, and the unavailability of microchips and plastics prevented companies from delivering finished goods and even services. This may help explain that while revenues and earnings are up, new business development is becoming increasingly difficult for companies surveyed, with the subsegment BRI falling sharply into contractionary territory of 36.1 in August from 51.7 in June.

These delays and disruptions not only hurt the companies that depend on raw materials and intermediate goods, they also directly impact the more than 54,000 people employed in San Diego’s Transportation and Logistics value chain. Furthermore, supply chain disruptions to San Diego companies hinders their ability to serve customers across the world. San Diego is a top 10 services-exporting metro, specializing in Professional, Scientific, and Technical Services like Research and Development (R&D), Cybersecurity, Engineering, and Software. These industries have massive impacts on the local economy with each 100 direct jobs supporting 200 more elsewhere in the region.

Remote work is driving companies to scale down office space

After more than 18 months of remote work, with multiple fits and starts to get back into the office, many companies are coming to terms with some form of permanent remote work for their staff. The high levels of efficiency gains reported in the June survey has since subsided but remain net positive and strongly so. Employers are not necessarily looking to further expand their remote work capabilities or adopt new technologies for remote work, but many report a high desire among their workforce to maintain remote work options. Several reports from across the country and industry show that workers are primarily interested in flexible work arrangements that allow them to go into the office as needed while being able to manage their personal lives and avoid unnecessary commutes when possible. This flexibility is especially important to working parents facing unpredictable school and daycare disruptions as the Delta variant causes classrooms to temporarily shut down, sending their children back home.

With fewer workers in the office full time, more companies are making the decision to reduce their physical footprint. Many Technology and Software companies report difficulty justifying large, empty offices and thus plan to scale down significantly over the next year. Even companies in Education and Healthcare, that serve customers in-person, are moving back-office workers to either hybrid or fully remote work environments.

However, there are still companies looking to add space. These are mostly concentrated in Life Sciences and Manufacturing, where strong sales and increased hiring require more room to accommodate this growth. While many of these companies indicated plans to add office space, even more need industrial and lab space for R&D. Currently, there is almost 7.7 million square feet of industrial and flex space available and nearly 19 million square feet of office available across the region. The growing needs of companies suggests the balance may need to shift in the other direction.

Whether pharmaceuticals or beer, San Diego companies have long produced the things that make life more comfortable and more enjoyable. These companies also drive economic growth in our region. It is important that they have the assets they need, both in terms of physical infrastructure and skilled talent, to grow and thrive in San Diego.

Stay tuned for more on San Diego’s changing business landscape. EDC will be back every other month with more trends and insights. For more data and analysis visit our research page.

Welcome to the third edition in EDC’s Changing Business Landscape Series, which will be published bi-monthly in the San Diego Business Journal and here on our blog. If you missed them, check out the March and May editions.

Surveying the changing business landscape in San Diego

The COVID-19 pandemic has impacted every facet of life, including how businesses operate. Companies in every industry are rapidly re-evaluating how they do business, changing the way they interact with customers, manage supply chains, and where their employees are physically located. This has massive immediate and long-term implications for San Diego’s workforce and job composition, as well as regional land use decisions and infrastructure investment.

To identify evolving trends in local business needs and operations, ensuring their ability to grow and thrive in the region, EDC is surveying more than 200 companies in the region’s key industries on a rolling basis throughout 2021 to monitor and report shifts in their priorities and strategies. In addition, EDC constructed the San Diego Business Recovery Index (BRI)—a sentiment index to measure companies’ perceptions of current conditions, as well as expectations for the future across several factors such as business development, employment and commercial real estate needs. (An index value >50 reflects expansion, and a value <50 reflects contraction. More information on the index and how it is calculated is available here.)

These insights will help inform long-term economic development priorities around talent recruitment and retention, quality job creation, and infrastructure development. Companies are surveyed on several topics, with varying emphases in each wave.

Here are three key findings from the third wave of surveying conducted in June 2021:

We are amid a great talent reshuffling. Businesses report increasing difficulty hiring and retaining talent, meanwhile the quits rate is at historic highs.

Supply chains remain knotted up. The strategic importance of our cross-border trade has never been clearer.

Space needs are in flux as companies prepare for return to office. Demand for office space may be waning, but life sciences companies are looking to add lab space.

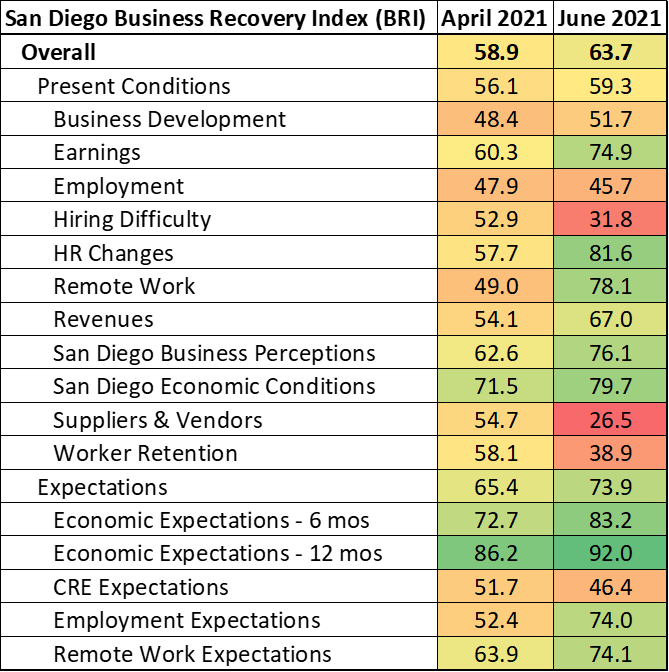

San Diego County firms built on the enthusiasm expressed in April’s survey, with the BRI advancing from 58.9 in April to 63.7 in June. The topline index was pulled higher by more upbeat views of, both, present conditions and expectations for the future. The present conditions index segment rose from 56.1 in April to 59.3 in June while the expectations segment climbed from 65.4 to 73.9 during that time. Business respondents in the region confirmed several trends that have made headlines recently. Companies stated that business conditions have improved significantly over the past two months (due in no small part to California’s reopening in June) while also noting that sourcing talent and suppliers has become significantly more difficult.

A great talent reshuffling

Companies reported that revenues and earnings have improved since April and thus optimism over the next six to 12 months has increased. Expectations are also strong in San Diego’s Innovation cluster. Businesses in this group conveyed that they plan to hire more aggressively in the coming months. This is particularly good news, since each new Innovation job supports another two jobs elsewhere in the regional economy.

Nonetheless, companies also reported having a tougher time attracting new talent as well as increased difficulty retaining existing workers. There has been much ado about labor shortages and the impact of increased and extended unemployment benefits, but the data show that there is a much more nuanced story. First, there is a large mismatch between the talent in-demand and the talent available to work. As of May (most recently available data at time of writing), there were 104,400 people unemployed in the San Diego region and more than 115,000 job openings. However, the top hiring industries are Administrative and Support Services, Professional Services and Manufacturing industries (nearly 40 percent of unique postings), whereas the bulk of the unemployed come from Leisure and Hospitality.

Second, there are record numbers of workers quitting their jobs. The Bureau of Labor Statistics measures the proportion of workers who voluntarily leave their job relative to total employment. This “quit rate” sat at 2.5 percent in May 2021 after falling from 2.8 percent in April—the highest ever recorded. The Conference Board survey’s labor market differential, another measure of views on whether jobs are plentiful or hard to get, vaulted from 36.9 in May 2021 to 43.5 in June. That is the highest level since 2000.

All this quitting not only reflects confidence in the availability of work, but also the changing needs and desires of workers. The San Diego Association of Governments surveyed both employers and employees earlier this year and found that only 36 percent of employers expect to have one or more employees working from home at least one day per week. Meanwhile 44 percent of employees surveyed expect to work from home an average of 1.2 days per week. This difference in expectations partly reflects differences in opinion of how remote work has impacted productivity—only nine percent of employers reported increased productivity during the pandemic versus 48 percent of employees.

Flexibility will be key to keeping and attracting the best and brightest of workers. Perhaps the companies EDC surveyed understand this better than most, as they indicated both improved efficiencies from, as well as increased planned future utilization of, remote work technologies in June compared to April.

Investing in supply chains locally, binationally

Hiring challenges are also impacting supply chains globally. Companies reported a sharp decrease in the accessibility and reliability of their suppliers and vendors. Here, BRI fell from 54.7 in April to a categorical low of 26.5 in June. This corroborates the headlines regarding shortages in lumber and microchips, which has in turn stalled production of higher end goods and led to spikes in commodity prices and other item such as used cars. A lot of these supply chain disruptions are temporary in nature, directly linked to safety measures and restrictions associated with pandemic (this is why longer-term inflation expectations remain stable).

Ports and businesses across the country have experienced ongoing shortages of labor, containers, truck chassis, and more; shipping vessels have been forced to wait in harbors, in some cases for more than two weeks. This global traffic jam has impacted schedule reliability so profoundly it has forced companies to revisit the ways in which they manage risk. Many companies have moved from a just-in-time strategy to just-in-case. This means firms now keep additional inventory on hand, anything from raw materials to the final product. The lack of supply and rising costs have disproportionately impacted small and mid-market suppliers and buyers. This has resulted in direct capital investment from smaller buyers into smaller suppliers to stabilize supply chains and build necessary redundancies.

The pandemic-induced constraint on the movement of goods has only exacerbated trends from the past few years. Trade wars, changing consumer behavior, and e-commerce were already disrupting global supply chains, all of which has highlighted the strategic importance of supply chain management as well as the region’s bi-national assets. The Cali Baja Binational Mega Region is already vertically integrated in Manufacturing, and a warehousing boom in Otay Mesa is increasing capacity for goods coming via land and sea. Cali Baja is an ideal location for companies that want to move operations closer to home but maintain a binational advantage. Continued investment in trade infrastructure, such as our ports of entry and direct route service, will further cement Cali Baja as a binational innovation hub.

The return to office will be in a lab

Back in April, companies indicated a modest desire to increase their physical footprint upon returning to the office. However, companies appear to be less sure as the return approaches. In June, companies expressed plans for a net reduction of space, but a deeper dive into the responses reveals that it is demand for office space that is waning. In fact, there is increasing demand for commercial space—life sciences companies in need of laboratory space. This reflects the influx of investment and rapid hiring we are seeing in these industries, as they lead the fight against the global pandemic. Fortunately, there is nearly 10 million square feet of industrial and flex space across San Diego County currently available for lease or purchase that could potentially accommodate this demand. Current hot spots include Sorrento Valley, Vista, and Otay Mesa; Downtown San Diego is also building capacity rapidly.

The headline story is a positive one for San Diego’s economy, but sentiment is far from identical across business sizes and industries. For example, small companies with fewer than 50 workers logged BRI of 53, which is modestly in expansionary territory, while companies with 250 or more employees measured an index value of 63.7. This makes sense, because San Diego’s Leisure and Hospitality businesses tend to be smaller establishments and were the hardest hit during the pandemic. While companies are enthusiastic to get back to full capacity and add workers, it will likely take a few more months for supply chains and the labor market to normalize again. The pandemic is a generational disruption with widespread ramifications, accelerating several trends already underway, including how and where people are willing to work.

Stay tuned for more on San Diego’s changing business landscape. EDC will be back every other month with more trends and insights. For more data and analysis visit: sandiegobusiness.org/research.

Every quarter San Diego Regional EDC analyzes key economic indicators that are important to understanding the regional economy and the region’s standing relative to the 25 most populous metropolitan areas in the U.S.

EDC explains San Diego’s Q2 2021 economic data:

Key Findings from Q2 2021:

VENTURE CAPITAL: Investment into Technology companies more than quadrupled. More than $2.4 billion in venture capital went to San Diego Tech companies during Q2, a 433 percent increase from the previous quarter and the first time that Tech received more VC funding than Life Sciences since Q1 2019. Life Sciences funding fell from record levels, but still pulled in more than $1.9 billion during the quarter, more than doubling the amount received in the same quarter last year. *Correction: Dollar values for Venture Capital in the preceding paragraph include other sources of funding, such as IPOs, mergers, and Acquisitions.

COMMERCIAL REAL ESTATE: Demand for office space jumps as State lifts lockdowns. Net absorption of office real estate was positive during the quarter, up more than 330,000 square feet, for the first time since Q4 2019 as San Diego businesses began transitioning back to the office. Additionally, Tech companies such as Apple and AppFolio are expanding their San Diego footprint, helping push office vacancy rates down and rent growth back up.

EMPLOYMENT: Job growth returns amid continued battle for talent. San Diego’s Q2 employment reversed the past year’s downward trend as the vaccine rollout led to loosened restrictions on businesses and increased consumer confidence. Year-over-year total nonfarm employment increased by 17,700 in Q2, with Leisure and Hospitality leading the way. However, total employment remains about 100,000 jobs lower than pre-pandemic levels and some key industries, such as Healthcare, are in dire need of more workers.

EDC study quantifies the impact of AI in region’s Cybersecurity cluster

Today, alongside Cyber Center of Excellence (CCOE) and Booz Allen Hamilton, EDC released the second study in a series on the proliferation of Artificial Intelligence (AI) and Machine Learning (ML) within San Diego County’s key economic clusters. “Securing the Future: AI and San Diego’s Cyber Cluster” quantifies the economic impact of the region’s Cybersecurity cluster and explores the proliferation of AI and ML technologies being used to thwart cybercrimes, among other critical needs by the private-sector and government.

While the term “Cyber” has become household nomenclature only in the past decade or so, the industry dates back 50 years. As cyberattacks and ransomware threats on local mega-brands fill our headlines, and our digital and non-digital worlds further integrate, the importance of and need for Cybersecurity cannot be overstated.

Underwritten by Booz Allen Hamilton, the web-based study—cyber.sandiegoAI.org—includes a timeline on the history of Cybersecurity, a roster of recent Defense-Cyber contracts and subsequent job growth, details on the $3.5 billion economic impact of the Cyber cluster, and a set of recommendations for driving the use of AI and ML across the region.

“This series serves to spotlight the importance of AI-ML application within the region’s key industries—which contrary to popular belief—is helping drive productivity, job growth, innovation, and security here and around the globe. While there is work to be done in getting more San Diegans plugged into Cyber and related jobs, the industry has proven to be an engine of growth, even despite disruptions brought on by COVID-19,” said Nate Kelley, Senior Research Manager, San Diego Regional EDC.

Key findings

The region’s Cyber companies are significantly more engaged with AI and ML technologies than firms in other industries. Cyber firms are developing AI at a rate 2.5 to three times the regional average. Moreover, half of all Cyber companies implemented AI at least three years ago compared with 43 percent across all industries.

AI has generated unparalleled productivity gains. Productivity in the Cyber cluster has grown 7.5 percent since 2018, nearly triple the average for all San Diego industries, thanks to the development and adoption of AI.

AI is producing jobs, not eliminating them. Some 61 percent of Cyber businesses plan to hire workers—including AI specialists—in the next year. Moreover, AI has helped the industry to sidestep chronic labor shortages by automating tedious, repeatable tasks and allowing current workers to do more with their time.

Talent shortages abound. Despite industry employment growing by 7.4 percent since 2018, 80 to 90 percent of local Cyber companies cited difficulty sourcing qualified workers. The region’s colleges and universities are expanding their course offerings to bridge these gaps, but more must be done to better draw students to these programs.

Home to the largest concentration of military assets in the world, San Diego—and its Cyber firms—are positioned for growth. Nearly three in five local Cyber firms work directly or indirectly for the federal government, including the Department of Defense, and 32 percent focus exclusively on fulfilling federal contracts. Defense contracts are typically big, multiyear investments that provide stability to San Diego’s Cyber industry.

“It should come as no surprise that San Diego is at the heart of transforming the defense industrial base leveraging today’s latest technology, while working to mitigate the risks inherent to increased connectivity and data-centric decision making,” said Jennie Brooks, Senior Vice President at Booz Allen Hamilton—underwriter of the EDC study series—and leader of the firm’s San Diego office, which employs over 1,200 professionals working on cybersecurity, analytics, engineering and IT modernization. “It’s clear that 5G, AI, ML, and cyber warfare will define our future battlefields, digital, and physical—and while we are encouraged by the report findings, we must all be ready to meet this new mission by fostering Cyber-ready tech talent, investing in up-skilling and reskilling programs, implementing rigorous cyber hygiene practices from the board level down, and coming together as a regional cluster to define how these new technologies will further—and safely—shape the San Diego region in the coming years.”

Cyber is an important and rapidly growing piece of the San Diego regional economy. Notably, every Cyber job generates another job in other industries in the region. The cluster accounts for 24,349 San Diego jobs across 874 firms, and has a total economic impact of $3.5 billion annually. This is about the equivalent of nine Super Bowls or 23 Comic-Cons.

“San Diego’s premier educational institutions, diverse industry base and robust federal assets seed not only the Cyber workforce but the innovation needed to protect our nation,” said Lisa Easterly, President & CEO, CCOE.

The study series is underwritten by Booz Allen Hamilton and produced by San Diego Regional EDC. The report was unveiled at a virtual, community event (video recording below) sponsored by CCOE and Thermo Fisher Scientific, with representatives from Booz Allen Hamilton, ESET, Analytics Ventures, Cal State San Marcos, and Naval Information Warfare Center Pacific, among others.

Welcome to the second edition in EDC’s Changing Business Landscape Series, which will be published bi-monthly in the San Diego Business Journal and here on our blog. If you missed the first edition, read it here.

Surveying the changing business landscape in San Diego

The COVID-19 pandemic has impacted every facet of life, including how businesses operate. Companies in every industry are rapidly re-evaluating how they do business, changing the way they interact with customers, manage supply chains and where their employees are physically located. This has massive immediate and long-term implications for San Diego’s workforce and job composition, as well as regional land use decisions and infrastructure investment.

To identify evolving trends in local business needs and operations, ensuring their ability to grow and thrive in the region, EDC is surveying more than 200 companies in the region’s key industries on a rolling basis throughout 2021 to monitor and report shifts in their priorities and strategies. In addition, EDC constructed the San Diego Business Recovery Index (BRI)—a sentiment index to measure companies’ perceptions of current conditions, as well as expectations for the future across several factors such as business development, employment and commercial real estate needs. Review the BRI concept and methodology here.

These insights will help inform long-term economic development priorities around talent recruitment and retention, quality job creation and infrastructure development. Companies are surveyed on several topics, with varying emphases in each wave.

Here are three key findings from the second wave of surveying conducted in April 2021:

The worst of the pandemic is behind us. Companies are very bullish about the next six to 12 months and, as a result, plan to accelerate hiring.

San Diego’s innovation cluster is (mostly) booming. Life Sciences companies lead the way while Cyber and Aerospace firms are still working through pandemic-related challenges.

Companies are seriously reevaluating their space needs. Smaller firms are looking to expand their footprint, while traditional Tech companies may be scaling down.

The worst is behind us

San Diego companies indicated that they think the worst of the pandemic has passed. With a BRI of 58.9 in April, regional firms noted that they plan to hire or rehire workers at a slightly faster pace than they have up to this point, while also expanding remote work capabilities going forward.

Last month’s index reading reflects bullish assessments of, both, present conditions (the present conditions subindex registered a value of 56.1) and expectations for the future (subindex of 65.4). Companies noted some lingering effects from a full year in lockdown, including difficulties with business development and job losses, and neutral to slightly negative feelings on remote work over the past year. Nonetheless, firms reported bright views on the current state of the regional economy and noted that San Diego businesses and key industries have adapted to the pandemic better that those in peer regions.

Regional companies were even more upbeat when it came to expectations for the future. All of the index’s expectations subindex values were north of 50, and companies overwhelmingly believe that the regional economy will have improved significantly in the next six months (subindex of 72.7) and even more so within the next 12 months (subindex of 86.2). This is important because many companies make decisions today based on their assessments of business conditions in the near future.

Most companies shared in the optimism, but to varying degrees. Small companies with fewer than 50 employees that were hardest hit during the pandemic held slightly dimmer, though still generally positive, views than their larger counterparts. In particular, smaller firms cited ongoing difficulties accessing new customers, managing suppliers and vendors, and hiring and retaining workers. Even so, assessments of current earnings trends were only slightly negative, and small firms held a sunny disposition when it comes to the current state of the San Diego economy and business climate.

Interestingly, however, companies with fewer than 50 workers had the highest level of optimism for the future across business size cohorts, which could signal an inflection point for the pace of hiring in the coming months. This bodes especially well for the jobs recovery heading into the second half of 2021, as 96 percent of San Diego’s businesses have fewer than 50 employees and small businesses have historically accounted for roughly half of all job growth.

San Diego’s innovation cluster is (mostly) booming

San Diego’s innovation cluster overwhelming expressed optimism entering 2021, as companies shifted toward meeting the demand for life-saving technologies, treatments and personal protective equipment leading to record venture capital investment and renewed job growth. However, a closer look reveals mixed results within the cluster. Industries like Cleantech, Software and Biomedical Device producers all held especially confident views (BRIs in the mid-60s), while Telecommunications, Cybersecurity and Aerospace each signaled ongoing challenges from the pandemic (BRIs ranging from 43 to 50).

Biotech and Biomedical Device manufactures hold strong expectations for the regional economy, with plans to increase their headcount and real estate footprint during the next year. In addition, they expect to increase their use of remote work over the same time frame. While this may seem contradictory, it reflects the modifications and enhancements that many companies are making to protect workers on the production floor, as well as those necessary to attract workers back into the office. Workers want to feel safe once back on company property and they also want to maintain the flexibility that working remotely has provided. To accommodate these needs, employers are preparing for a flexible or hybrid workplace once reopen. In addition, many companies are reconfiguring and even seeking new space to keep workers spread out, adapting space to be more comfortable in a post-pandemic environment. This includes ‘hoteling’ and ‘neighborhooding’ models to help reduce the flow of people and simultaneously allow teams to collaborate in person. Companies are preparing for a gradual return to the office to give workers adequate time to warm up to pre-pandemic routines. More on that below.

While Telecommunications and Cybersecurity firms all share this optimistic regional economic outlook with their Life Sciences peers, these industries are much more subdued about their own expansion plans for the next year. On net, they see their needs for space as unchanged, with some modest reductions in hiring compared to typical years. This reflects the challenges these industries have faced during the pandemic, namely with respect to increased difficulty with sales, hiring and, somewhat surprisingly, inefficiencies from remote work. Aerospace has not yet recovered from the initial impacts of the pandemic, still reeling from significant hits to both sales and employment, as well as disruptions in their supply chains from lockdowns and restricted international travel and transportation.

Smaller firms are looking to add space

After more than a year of implementing remote work and reduced onsite staffing, companies are beginning to plan for a return to the office. However, how much space awaits those returning to the office will vary by industry as well as firm size.

It is small- and medium-sized firms that are looking to expand their commercial real estate footprint over the next year rather than larger firms. In fact, the proportion of firms surveyed that expect to increase space by 10 percent or more of their current square footage is nearly double that of those planning to reduce their current space by 10 percent or more (16 percent to 8.4 percent, respectively). However, when you factor in the size of each company, those planning significant real estate growth represent only three percent of the jobs compared to 13 percent of jobs for those looking to reduce space significantly (companies surveyed collectively employ nearly 200,000 workers).

When we look at the innovation companies, we see some stark differences between traditional Technology and Biotechnology industries. Eight percent of respondents representing 22 percent of jobs plan to reduce their space by more than 10 percent—mostly in the Telecommunications industry. However, nearly 26 percent of respondents representing 41 percent jobs expect to add modest amounts of space less than 10 percent of their current footprint. Here many respondents are in the Biomedical Device and Biotech industries and likely in need of additional production or lab space.

Understanding these evolving and distinct trends is important because San Diego’s innovation cluster is leading the region out of this pandemic-driven economic downturn, just as it has in each past downturn. Each job added in the innovation cluster supports another two jobs elsewhere in the economy. Yet, these innovation companies do not necessarily need to be physically located in San Diego in order to operate. Making sure these companies have the infrastructure and access to talent that they need to flourish is critical to our region’s prosperity.

Stay tuned for more on San Diego’s changing business landscape. EDC will be back every other month with more trends and insights. For more data and analysis visit: sandiegobusiness.org/research.

Every quarter San Diego Regional EDC analyzes key economic indicators that are important to understanding the regional economy and the region’s standing relative to the 25 most populous metropolitan areas in the U.S.

EDC explains San Diego’s Q1 2021 economic data:

Key Findings from Q1 2021:

COMMERCIAL REAL ESTATE: Offices aren’t going anywhere. Regional shutdowns and new remote-work policies due to the COVID-19 pandemic have changed the nature of office space. While increased office vacancy (14.2 percent during Q1) suggests companies were abandoning their current offices, a recent survey of San Diego employers found that 39 percent plan to rent, lease, or purchase additional space in the next 12 months. Companies in the region’s innovation industries have more than recovered job losses from the early months of the pandemic and are looking to return to the office in some capacity over the coming months as health guidelines permit.

VENTURE CAPITAL: Biotech leads venture capital investment. In Q1, San Diego saw $2 billion in venture capital (VC) investment come into the region by way of 59 deals—the highest number in a quarter since 2000. The top three deals were worth nearly $1.2 billion, all to local biotechs Mesa Biotech, Fate Therapeutics, and Blacksmith Medicines, and account for more than half of all VC investment in the region. These continued VC inflows are a testament to San Diego’s position as a global life sciences leader.

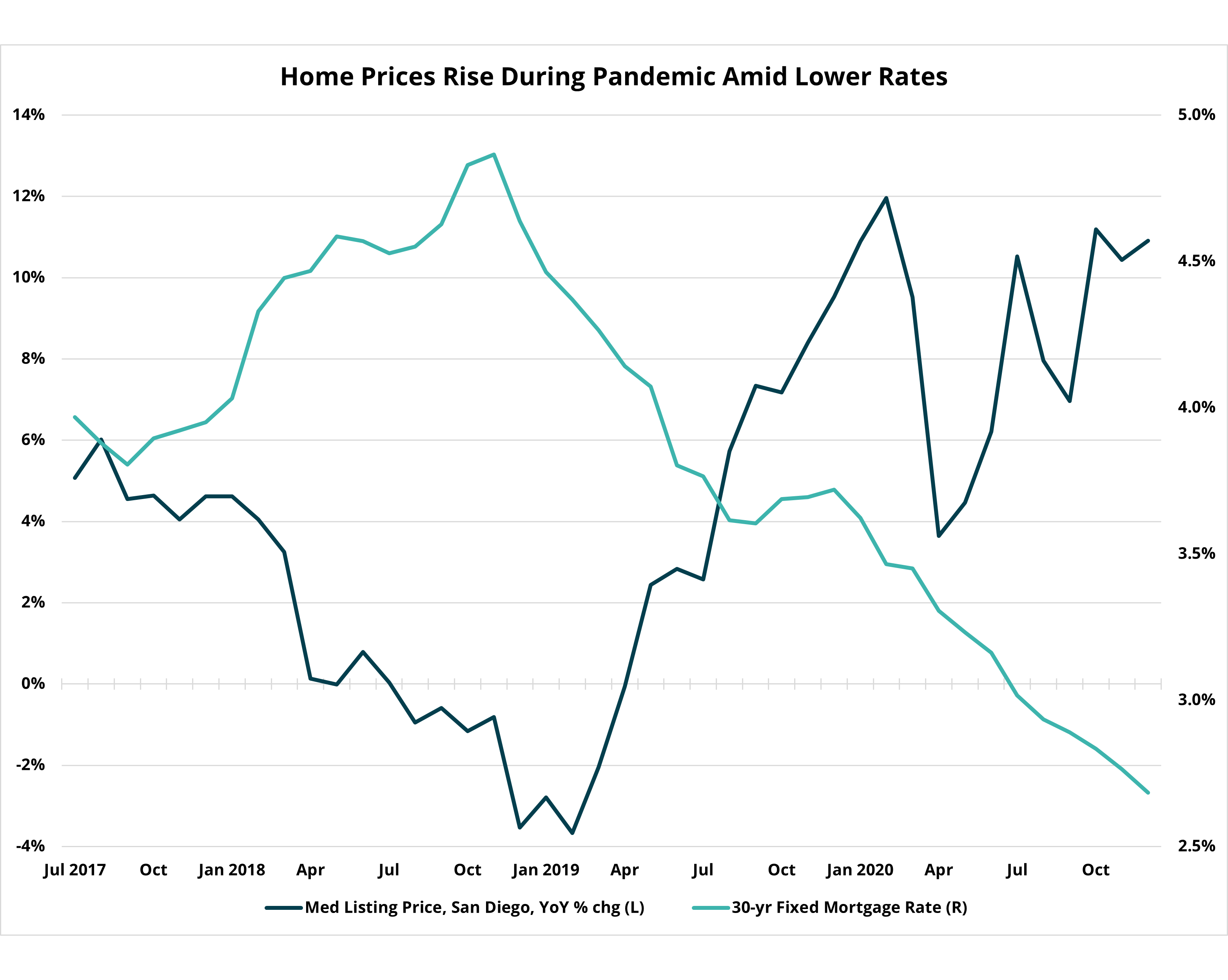

HOUSING: Rising home prices further hinder affordability. The median home price in Q1 was $763,500—a historic high that has continuously climbed during the pandemic, despite job losses and economic uncertainty. Increasing home prices make it difficult for new homebuyers to enter the market. We can hope that increased vaccinations will encourage sellers off the sidelines and free up more inventory for buyers.

San Diego Regional EDC is excited to kick-off our Changing Business Landscape Series, which will be published bi-monthly in the San Diego Business Journal and on our blog.

Surveying the changing business landscape in San Diego

The COVID-19 pandemic has impacted every facet of life, including how businesses operate. The San Diego region began the year with near-record high unemployment and widespread small business closures. Meanwhile, large companies across the globe have extended remote work well into 2021 and are even abandoning their corporate campuses. Companies in every industry are rapidly re-evaluating how they do business and changing the way they interact with customers, manage supply chains, and where their employees are physically located. This has massive immediate and long-term implications for San Diego’s workforce and job composition, as well as regional land use decisions and infrastructure investment.

To identify evolving trends in local business needs and operations, ensuring their ability to grow and thrive in the region, EDC began surveying more than 200 employers in the region’s key industries in January. Given the uncertainty of this moment in history, EDC will continue to survey these companies on a rolling basis throughout 2021 to monitor and report out shifts in their priorities and strategies. These insights will help inform long-term economic development priorities around talent recruitment and retention, quality job creation, and infrastructure development. Businesses are surveyed on several topics, with varying emphases in each wave.

Here are three key findings:

Everything is different, yet the future is bright. The pandemic has fundamentally altered how businesses operate across key industries. However, most companies are optimistic about their ability to pivot and emerge even stronger.

Remote working is no longer a perk or competitive advantage—it’s the standard. Most companies view remote working as here to stay. This is viewed as both a benefit and as a threat to employee retention.

Long commutes have been replaced by a blurring of work-life boundaries. Companies are struggling in maintaining employee morale and engagement. While many are seeing signs of employee burnout and isolation, few report significant concerns with retention.

San Diego’s innovation cluster rises to meet the challenge

One year into a global pandemic, San Diego’s most innovative companies and industries are well on their way to economic recovery. In fact, high-wage jobs—many of which are concentrated in aerospace, life science, and technology industries—have more than recovered from the pandemic-driven recession. This is welcome news as these are key drivers of economic growth in the region. In fact, every “innovation” job supports another two jobs elsewhere in the economy.

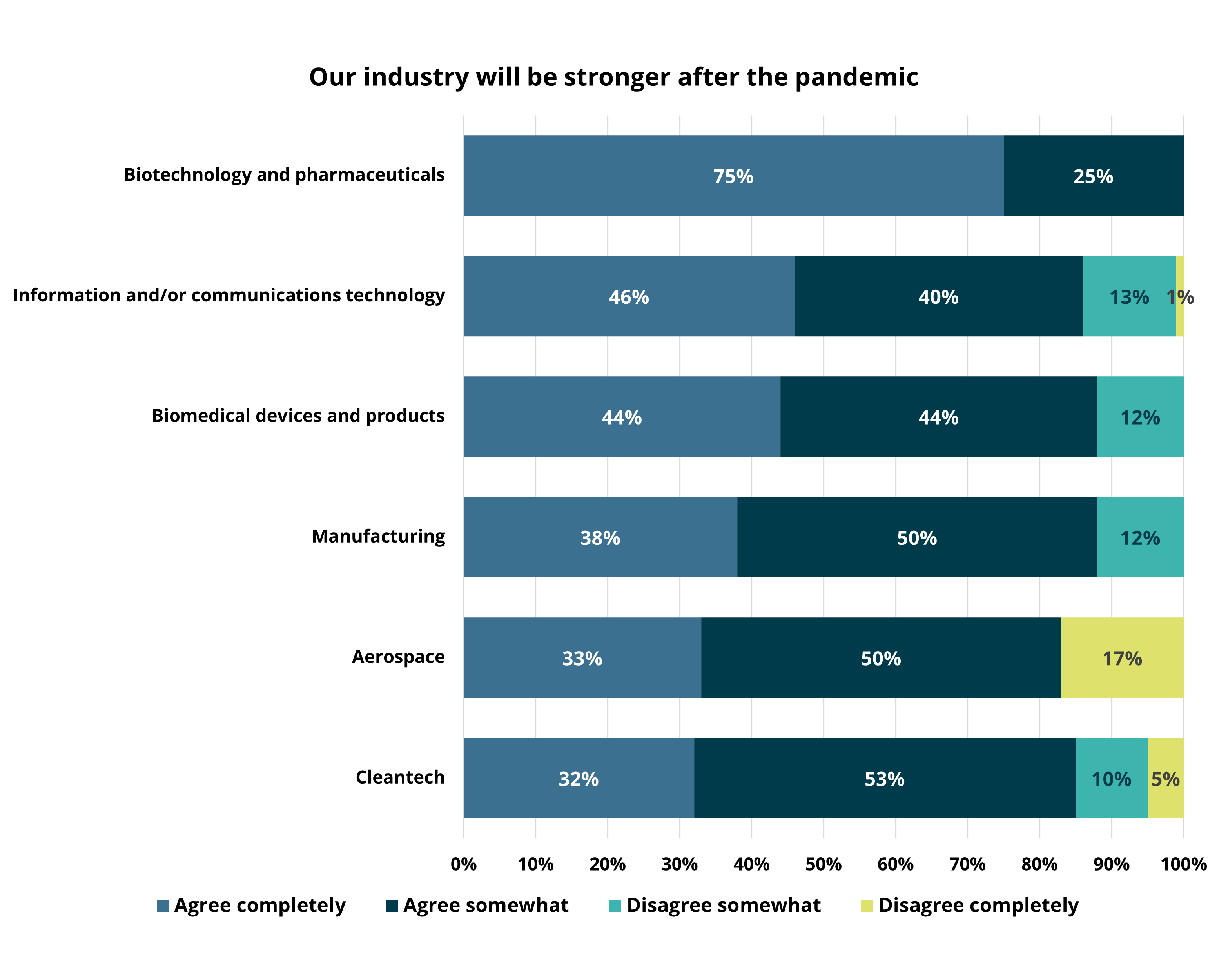

Even though growth has returned to the innovation cluster, the pandemic has disrupted the way these companies operate. The overwhelming majority (83 percent) of companies surveyed agree that the pandemic has fundamentally altered their industry. Yet, nearly as many (81 percent) feel that their industry has been able to adjust and remain healthy. Even more encouraging, 87 percent believe their industry will emerge even stronger once the pandemic has ended after adopting new ideas and implementing new strategies. However, those in the aerospace industry express somewhat lower levels of optimism, as the industry faces continued uncertainty around travel safety and demand.

Confidence is somewhat lower among smaller firms. Only 77 percent of those with fewer than 50 employees agree that their industry would emerge stronger and 10 percent strongly disagree. This likely reflects the disproportionate impact that the pandemic has had on small businesses, regardless of industry. While those in leisure and hospitality have certainly been the hardest hit, even small firms in professional and business services, including scientific and technical services, are currently experiencing lower revenues compared to before the pandemic.

Yet, the strongest signal for optimism comes from the direct response in combatting the novel coronavirus. San Diego companies have been among those leading the fight in everything from personal protective equipment and diagnostics to therapeutics and vaccine development. The life-changing and life-saving companies have pivoted and innovated yet again, drawing in record levels of venture capital investment. In the fourth quarter of 2020 alone, the region received nearly $2.7 billion in venture funding—with almost three-quarters going to life sciences and healthcare companies—which is more than three previous quarters combined, and $2 billion more than Q4 2019. The surge in investment and jobs recovery has the majority of innovation companies confident in the region’s ability to grow in prominence, or remain steadfast as a global leader in tech and life sciences.

The war for talent has no bounds

Talent has always been San Diego’s competitive advantage. People come from all over the world to get educated and build meaningful careers in everything from software engineering and autonomous vehicles to genomics sequencing and cybersecurity. San Diego’s innovation industries are among the highest-paying and fastest-growing in the region. Despite a global pandemic, many of these industries are accelerating hiring. The information sector, including telecommunications and information technology services, posted 20 percent more unique job ads in December 2020 than the year prior.

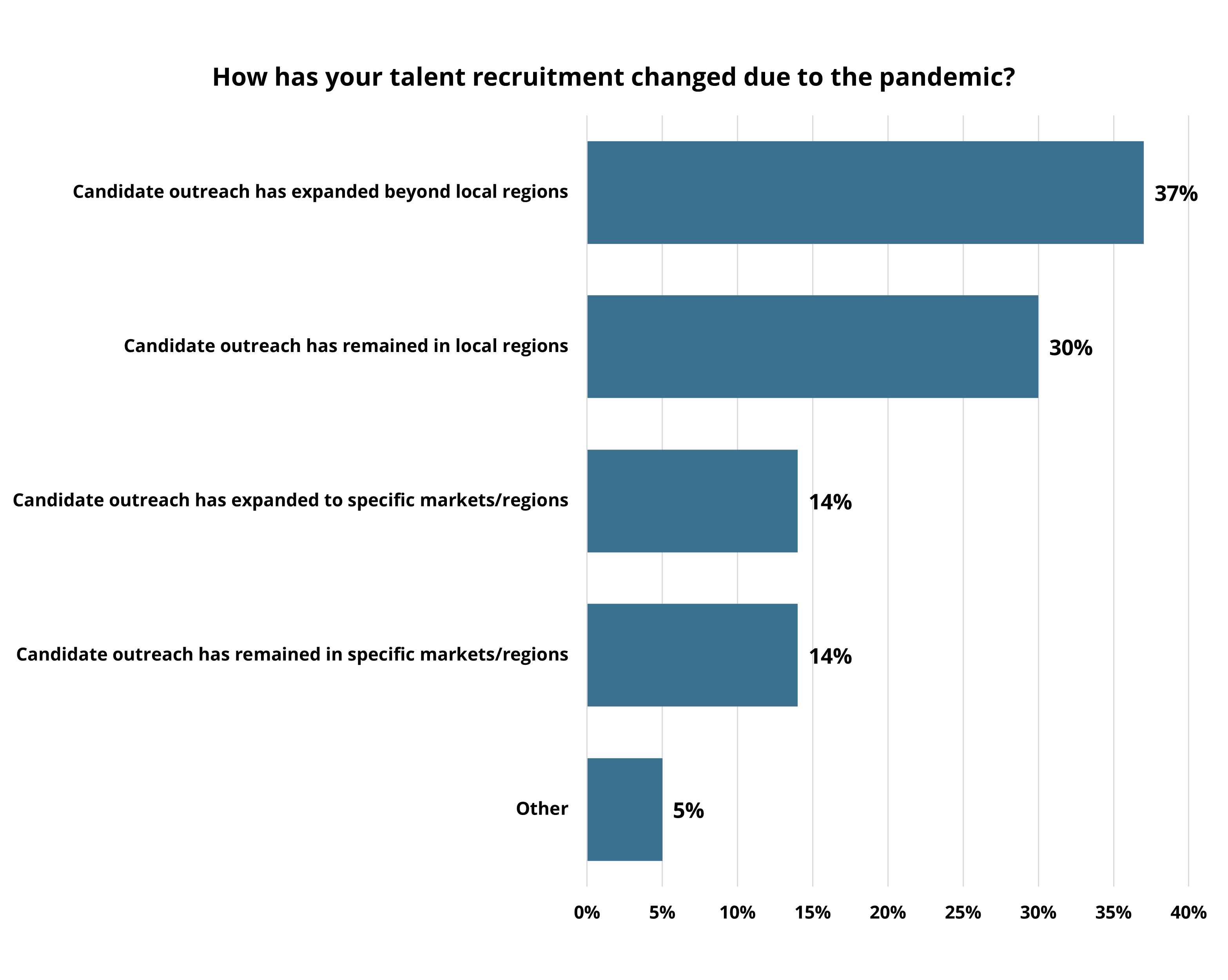

However, top talent remains hard to find. And while many of the jobs in these industries have shifted to either partially or fully remote, there are mixed feelings about whether it is a benefit or a detriment to talent recruitment and retention. Perceptions are tied to a company’s approach to attracting remote talent (see below). On one hand, a majority of respondents think that their ability to hire and retain skilled talent will not be impacted by the pandemic because of remote work capabilities. Many have expanded their recruitment beyond San Diego’s borders and are willing to accommodate working from outside the region to retain the very best talent. These San Diego-based companies that view the world as their pool for talent are embracing a global workforce that can get the job done from anywhere.

Yet, there is also a large minority of companies that view the pandemic as impacting the way they hire and retain talent. Again, the shift to remote work is cited as the top reason, with an even larger proportion (35 percent) identifying it as the cause for their pessimism. In fact, 45 percent of survey respondents rate hiring new employees during the pandemic as either “difficult” or “more difficult” than before, compared to 18 percent who view it as “easier” or “much easier.” Furthermore, nearly half of respondents cite talent recruitment as an area needing assistance and 20 percent identify it as an “urgent need.”

The pandemic has leveled the playing field for markets aiming to attract the best and brightest knowledge. San Diego’s competition with companies and regions across the country has increased. The region’s high cost of living is by far the biggest impediment to talent attraction, with 44 percent of respondents identifying high home prices as the most negative attribute of the San Diego market. This is due in large part to housing production not keeping pace with employment growth. As a result, San Diego has the second highest median home price among the 25 largest metros in the U.S., behind only San Francisco, and home prices jumped another 11 percent in 2020. Ensuring San Diego is an attractive and affordable place for talent and business is critical to maintaining its regional competitiveness.

Responding to workers’ needs is top of mind for companies

Transitioning to a remote work environment has been challenging. Business leaders are acutely aware of the need to balance conducting business as usual and responding to the changing needs of a newly remote workforce. Survey respondents report signs of ‘zoom fatigue,’ blurred work-life boundaries, and isolation among employees. While it has not yet significantly impacted retention, a full 60 percent of respondents rated “maintaining employee morale” as more challenging during the pandemic.

Furthermore, respondents expressed concerns about returning to an in-person work environment, recognizing that not all employees will want to return to the office immediately or full-time. This next phase of work will bring about a new set of challenges and a need for new policies, systems, and support for San Diego workers. Many questions remain around how much space will be needed and how it might need to be reconfigured to accommodate a flexible work environment that is also responsive to new health and safety requirements.

Survey respondents rated individualistic factors related to professional growth and work-life balance as the most important attributes to a competitive market for talent attraction and retention. This differs greatly from perceptions from just four years ago, when top universities and an entrepreneurial spirit were more top of mind. The desire to adapt and respond to the most pressing needs of its workforce, reinforces the notion that San Diego businesses value talent above all else.

Stay tuned for more on San Diego’s changing business landscape. EDC will be back every other month with more trends and insights. For more data and analysis visit: sandiegobusiness.org/research.

A marketing initiative of EDC and the five cities along the 78 Corridor, Innovate78 serves to spotlight the businesses and innovators that make our region competitive.

Today, Innovate78 released a new report, The Future of Manufacturing in North County, which finds the industry will continue to prove its resiliency and positive economic impact in the region—even amid trends in automation, globalization and COVID-19 ramifications. According to the study, manufacturing accounts for $18 billion annually (or seven percent) of the area’s economy, and while many of the 813 local manufacturing firms were impacted by coronavirus, 58 percent of survey respondents are looking to increase their space.

The study analyzes trends in employment, which is concentrated in high-value goods like computer and electronic product manufacturing. This sub-industry specifically accounts for nearly one-third of all manufacturing jobs in North County, with 12,746 employees of the total 40,151 jobs reported in the study. This number is expected to grow nearly six percent in the next five years—continuing to position manufacturing as a key driver of North County’s economy.

Flux Power, a company represented in the study that manufactures advanced lithium-ion battery for industrial and commercial equipment, increased both their staff and revenue in 2020 amid the pandemic. With more than 100 employees, the Vista-based company is now looking to increase both its production and nonproduction space within the region.

“The need to be efficient, safe and environmentally-conscious is high, especially now, as businesses plan for post-COVID-19 recovery,” said Chuck Scheiwe, chief financial officer of Flux Power. “Manufacturing products that empower others to improve their day-to-day efficiencies will be critical in our industry and region’s future growth, and we’re proud to be part of it.”

The study reports that during COVID-19, North County manufacturing companies were undoubtedly impacted by the pandemic, with 43 percent of respondents reporting a loss of revenue in 2020. Looking at net growth, however, there was a reported one percent increase in manufacturing jobs, with 186 manufacturing jobs lost and 956 gained as noted by respondents. Most job losses were in medical manufacturing, while most job gains were in machinery manufacturing.

One company that reported job gains is Quik-Pak, an Escondido based computer and electronic manufacturing company. In addition to anticipating upscaling facilities in the future, during COVID-19 Quik-Pak hired staff and reported increased revenue.

“The strength of the manufacturing industry in North County San Diego is one of the reasons we wanted to expand here,” said Rosie Medina, vice president sales and marketing of Quik-Pak. “The talent pool is rich, and there is space to grow. We appreciate that not every region has both of these critical components that are needed for our industry to thrive.”

Automation, globalization and COVID-19 are obvious pressures affecting North County’s manufacturing industry. However, as Quik-Pak and Flux Power note, the need for innovation and talent remain strong. There are 9,804 manufacturing jobs with a higher-than-average risk of automation—that’s nearly 24 percent of all North County manufacturing jobs. Investment in upskilling and re-training will be needed to help move these workers into other quality jobs over time.

“From craft beer to surfboards, to life-changing medical devices and technology services, manufacturing has long been a pillar of the region’s economy, with impacts spanning beyond our community,” said Jordan Latchford, research manager of San Diego Regional EDC, the study author and managing entity of Innovate78. “This study confirms the manufacturing industry in North County is poised for a strong recovery, and will remain a significant economic driver for the San Diego region.”

EDC study quantifies the impact of increased local procurement

Today, as part of a commitment to inclusive economic recovery, EDC released a study and set of recommendations for large employers to support small businesses by buying local. “Anchor Institutions: Leveraging Big Buyers for Small Business“ analyzes the spend of more than a dozen local anchors and demonstrates the impact of increased local procurement on quality job creation.

Anchor institutions are defined as universities, hospitals, local government agencies, the U.S. Navy and other large employers that are physically bound to the region.

In San Diego, anchors represent eight of the region’s 10 largest employers—providing more than 72,000 jobs. They purchase tens of billions of dollars in goods and services every year, and yet, local anchors send about one-quarter of all procurement spend outside the region.

The web-based study—procurelocal.inclusivesd.org—includes a summary of local spending, a cluster map of anchor institutions in the region, estimated economic impact from increased local spending, and a set of recommendations for growing quality jobs across San Diego through procurement.

The COVID-19 pandemic has disproportionately impacted people of color and spurred the closure of one-in-three small businesses across San Diego. Local small businesses employ nearly 60 percent of the total workforce, which is double the national average, and are responsible for nearly half of all job growth in the last five years. Despite their critical importance to the region’s economy, many small businesses report struggling to attract customers and generate new sales.

“Small business resiliency will be key in getting this recovery right. This report further demonstrates the importance of connecting our region’s small and diverse businesses to large, institutional buyers,” said Eduardo Velasquez, EDC Research Director. “This will mean more quality jobs for San Diegans, more thriving businesses and a stronger regional economy.”

KEY FINDINGS

Collectively, 14 anchors surveyed spend more than $9.9 billion each year on a range of goods and services, and only about $247 million of this reported spend can be traced back to San Diego businesses. Further, only a small proportion of this spend is reaching small (14 percent) and minority-owned or diverse businesses (11 percent).

Small shifts in procurement can mean big economic impact:

If the 14 anchors surveyed increased local construction spending by just one percent, it would put around $32 million into local construction businesses, adding $466 million to the local economy and helping create nearly 4,500 jobs in the region.

The same one percent increase in professional services (e.g. legal assistance) spending would pump nearly $12 million into local suppliers, resulting in an economic impact of nearly $56 million and support another 800 jobs.

The majority of these new jobs would be in industries with a higher-than-average concentration of quality jobs (those that pay middle-income wages).

“As a large employer that works with many diverse suppliers to meet our mission of delivering clean, safe and reliable energy, SDG&E understands the value small businesses bring to the regional economy,” said Christy Ihrig, vice president of operations support, SDG&E, anchor event and study sponsor. “When they thrive, our region thrives. To support economic recovery from the pandemic, we are more committed than ever to grow our supplier diversity program and encourage other local employers to do the same.”

Beyond impacts to suppliers and the regional economy at large, anchor institutions that buy from local, small, diverse businesses also stand to benefit. Specifically, several local anchors note that setting goals for greater procurement from these suppliers has resulted in greater customer service, supply chain diversity and resiliency, and stronger brand equity in the communities they serve.

“‘Shop local’ is about more than individuals; it means big business and organizations choosing to support their neighbors by buying in their communities. The City of San Diego takes pride in its efforts to work with local companies, is seeking increased opportunities to buy local and implores other local organizations to follow suit. Together, this is how we ensure a more equitable and inclusive San Diego,” said Mayor Todd Gloria, City of San Diego, study sponsor.

A CALL TO ACTION

To maintain our regional competitiveness, we need to create 50,000 quality jobs in small businesses by 2030, as outlined in EDC’s inclusive growth strategy. To do that, it’s imperative we help San Diego’s small and diverse businesses recover and thrive.

San Diego needs its largest employers (and our largest buyers) to commit to redirecting their procurement to local, small, and diverse businesses. To do this we must:

identify spend areas with high potential for inclusive, local sourcing; and

define and track metrics that ultimately drive bidding processes.

We invite large firms to join San Diego Regional EDC’s Anchor Collaborative and help us shape and achieve this goal—join us here.

The report was unveiled today at the first in a series of Town Hall events. Watch a recording of the event here. Thank you to the study sponsors: SDG&E, City of San Diego, Civic Community Ventures, and the University of San Diego School of Business.